2025-08-29

Risk management is not simply about cutting losses or setting a stop-loss level. For professional traders, especially those preparing for or working with prop firms, the question is: How can I allocate capital so that each position contributes equally to portfolio risk, regardless of market volatility or asset class?

This concept is the foundation of Risk Parity Portfolio Construction. While risk parity is traditionally applied to multi-asset portfolios (stocks, bonds, commodities), forex traders can also leverage the same logic to stabilize returns and reduce the destructive impact of volatility clustering.

In this blog, we will explore how forex traders can implement risk parity, the tools required to calculate volatility-adjusted allocations, and how this method can align with prop firm rules.

Risk parity is a portfolio construction technique where allocation is based on risk contribution rather than capital contribution.

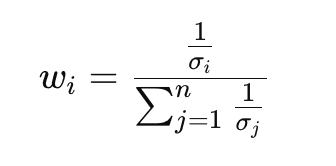

Mathematically, risk contribution is tied to volatility and correlation:

Forex markets are unique compared to equities:

Risk parity helps forex traders in three ways:

For prop traders, this is not just a theory—it directly affects survival in challenge phases and long-term capital management.

The foundation is calculating volatility for each pair. Traders often use:

Example:

If you allocate $10,000 equally, GBP/JPY contributes far more risk than EUR/USD. In risk parity, GBP/JPY’s allocation will be reduced.

Risk parity uses inverse volatility weighting:

Where:

This ensures that higher volatility pairs automatically get smaller allocations.

If two pairs are highly correlated (EUR/USD and GBP/USD), risk parity penalizes duplication. Traders often use a correlation matrix to reduce overlapping exposure.

Advanced methods include:

Forex traders often add leverage after achieving a balanced risk portfolio. For example:

This avoids the classic problem of under-leveraging low-volatility pairs like EUR/USD.

Choose a diverse basket—avoid over-concentration in USD majors. Example:

Use a rolling 20-day ATR or realized volatility.

Allocate according to inverse volatility.

Check correlation over a 60–90 day window. Reduce exposure to highly correlated pairs.

Match prop firm rules: don’t exceed daily drawdown risk.

Traders must monitor the portfolio dynamically and rebalance frequently.

Instead of fixed lookback windows, volatility is estimated adaptively—shorter during high volatility, longer during calm markets.

Forex pairs respond differently depending on global macro cycles. Risk parity can integrate regime detection models to allocate differently in “risk-on” vs “risk-off” markets.

ML models can predict volatility clusters, feeding into risk parity allocation. For example:

Assume a prop trader has $100,000 capital. They select 4 pairs:

Inverse volatility weights:

Final adjusted allocations:

Now, each pair contributes equally to total portfolio risk—protecting the trader from sudden shocks in USD/TRY or GBP/JPY.

Risk parity is not only quantitative—it also affects trader psychology.

Risk parity sits in the middle: practical, conservative, and adaptive.

For forex prop traders, building a risk parity portfolio is more than a theoretical exercise—it is a survival strategy. By ensuring each trade contributes equally to overall portfolio risk, traders reduce concentration risk, stabilize equity growth, and align with the stringent rules of funding firms.

Risk parity does not guarantee profits, but it maximizes risk efficiency, which is the ultimate currency for professional traders.

© 2025 iTrader Global Limited | 公司注册号 15962

iTrader Global Limited 位于科摩罗联盟安儒昂自治岛穆察姆杜 Hamchako,并受科摩罗证券委员会(Securities Commission of the Comoros)许可及监管。我们的牌照号为 L15962/ITGL。

iTrader Global Limited 以“iTrader”作为交易名称,获授权从事外汇交易业务。公司的标志、商标及网站均为 iTrader Global Limited 的专属财产。

风险提示: 差价合约(CFD)交易因杠杆作用存在高风险,可能导致资金快速亏损,并非适合所有投资者。

交易资金、差价合约及其他高杠杆产品需要具备专业知识。

研究显示,84.01% 使用杠杆的交易者会遭受亏损。请务必充分了解相关风险,并确认在交易前已做好承担资金损失的准备。

iTrader 特此声明,不会对任何个人或法人在杠杆交易中产生的风险、亏损或其他损失承担全部责任。

本网站提供的新闻及信息仅用于教育目的。用户应独立且审慎地作出金融决策。

限制条款: iTrader 不会向法律、法规或政策禁止此类活动的国家或地区居民提供本网站或相关服务。若您居住在限制使用本网站或服务的司法管辖区,您有责任确保遵守当地法律。iTrader 不保证其网站内容在所有司法管辖区均适用或合法。

iTrader Global Limited 不向以下国家/地区的公民提供服务,包括但不限于:美国、巴西、加拿大、以色列及伊朗。