2025-08-29

Risk management is not simply about cutting losses or setting a stop-loss level. For professional traders, especially those preparing for or working with prop firms, the question is: How can I allocate capital so that each position contributes equally to portfolio risk, regardless of market volatility or asset class?

This concept is the foundation of Risk Parity Portfolio Construction. While risk parity is traditionally applied to multi-asset portfolios (stocks, bonds, commodities), forex traders can also leverage the same logic to stabilize returns and reduce the destructive impact of volatility clustering.

In this blog, we will explore how forex traders can implement risk parity, the tools required to calculate volatility-adjusted allocations, and how this method can align with prop firm rules.

Risk parity is a portfolio construction technique where allocation is based on risk contribution rather than capital contribution.

Mathematically, risk contribution is tied to volatility and correlation:

Forex markets are unique compared to equities:

Risk parity helps forex traders in three ways:

For prop traders, this is not just a theory—it directly affects survival in challenge phases and long-term capital management.

The foundation is calculating volatility for each pair. Traders often use:

Example:

If you allocate $10,000 equally, GBP/JPY contributes far more risk than EUR/USD. In risk parity, GBP/JPY’s allocation will be reduced.

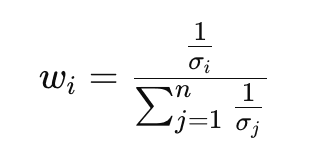

Risk parity uses inverse volatility weighting:

Where:

This ensures that higher volatility pairs automatically get smaller allocations.

If two pairs are highly correlated (EUR/USD and GBP/USD), risk parity penalizes duplication. Traders often use a correlation matrix to reduce overlapping exposure.

Advanced methods include:

Forex traders often add leverage after achieving a balanced risk portfolio. For example:

This avoids the classic problem of under-leveraging low-volatility pairs like EUR/USD.

Choose a diverse basket—avoid over-concentration in USD majors. Example:

Use a rolling 20-day ATR or realized volatility.

Allocate according to inverse volatility.

Check correlation over a 60–90 day window. Reduce exposure to highly correlated pairs.

Match prop firm rules: don’t exceed daily drawdown risk.

Traders must monitor the portfolio dynamically and rebalance frequently.

Instead of fixed lookback windows, volatility is estimated adaptively—shorter during high volatility, longer during calm markets.

Forex pairs respond differently depending on global macro cycles. Risk parity can integrate regime detection models to allocate differently in “risk-on” vs “risk-off” markets.

ML models can predict volatility clusters, feeding into risk parity allocation. For example:

Assume a prop trader has $100,000 capital. They select 4 pairs:

Inverse volatility weights:

Final adjusted allocations:

Now, each pair contributes equally to total portfolio risk—protecting the trader from sudden shocks in USD/TRY or GBP/JPY.

Risk parity is not only quantitative—it also affects trader psychology.

Risk parity sits in the middle: practical, conservative, and adaptive.

For forex prop traders, building a risk parity portfolio is more than a theoretical exercise—it is a survival strategy. By ensuring each trade contributes equally to overall portfolio risk, traders reduce concentration risk, stabilize equity growth, and align with the stringent rules of funding firms.

Risk parity does not guarantee profits, but it maximizes risk efficiency, which is the ultimate currency for professional traders.

© 2025 iTrader Global Limited | Company registration number 15962

iTrader Global Limited is located at Hamchako, Mutsamudu, Autonomous Island of Anjouan, Union of Comoros, The Comoros and is licensed and regulated by the Securities Commission of the Comoros. Our license number L15962/ ITGL

iTrader Global Limited, operating under the trading name “iTrader,” is authorized to engage in Forex trading activities. The company’s logo, trademark, and website are the exclusive property of iTrader Global Limited.

Risk Warning: CFD trading carries a high risk of rapid capital loss due to leverage and may not be suitable for all users.

Trading in funds, CFDs, and other high-leverage products requires specialized knowledge.

Research indicates that 84.01% of leveraged traders incur losses. Please ensure you fully understand the risks and are prepared to lose your capital before engaging in leveraged trading.

iTrader hereby states that it will not be held fully responsible for leveraged trading risks, losses, or other damages incurred by any individual or legal entity.

The news and information provided on this website are for educational purposes only. Users should make independent and informed financial decisions.

Restrictions: iTrader does not direct its website or services to residents of countries where such activities are prohibited by law, regulation, or policy. If you reside in a jurisdiction where the use of this website or its services is restricted, you are responsible for ensuring compliance with local laws. iTrader does not guarantee that the content of its website is appropriate or lawful in all jurisdictions.

iTrader Global Limited does not provide services to citizens of certain countries, including (but not limited to): the United States, Brazil, Canada, Israel, and Iran.