2025-08-29

Risk management is not simply about cutting losses or setting a stop-loss level. For professional traders, especially those preparing for or working with prop firms, the question is: How can I allocate capital so that each position contributes equally to portfolio risk, regardless of market volatility or asset class?

This concept is the foundation of Risk Parity Portfolio Construction. While risk parity is traditionally applied to multi-asset portfolios (stocks, bonds, commodities), forex traders can also leverage the same logic to stabilize returns and reduce the destructive impact of volatility clustering.

In this blog, we will explore how forex traders can implement risk parity, the tools required to calculate volatility-adjusted allocations, and how this method can align with prop firm rules.

Risk parity is a portfolio construction technique where allocation is based on risk contribution rather than capital contribution.

Mathematically, risk contribution is tied to volatility and correlation:

Forex markets are unique compared to equities:

Risk parity helps forex traders in three ways:

For prop traders, this is not just a theory—it directly affects survival in challenge phases and long-term capital management.

The foundation is calculating volatility for each pair. Traders often use:

Example:

If you allocate $10,000 equally, GBP/JPY contributes far more risk than EUR/USD. In risk parity, GBP/JPY’s allocation will be reduced.

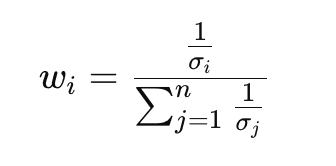

Risk parity uses inverse volatility weighting:

Where:

This ensures that higher volatility pairs automatically get smaller allocations.

If two pairs are highly correlated (EUR/USD and GBP/USD), risk parity penalizes duplication. Traders often use a correlation matrix to reduce overlapping exposure.

Advanced methods include:

Forex traders often add leverage after achieving a balanced risk portfolio. For example:

This avoids the classic problem of under-leveraging low-volatility pairs like EUR/USD.

Choose a diverse basket—avoid over-concentration in USD majors. Example:

Use a rolling 20-day ATR or realized volatility.

Allocate according to inverse volatility.

Check correlation over a 60–90 day window. Reduce exposure to highly correlated pairs.

Match prop firm rules: don’t exceed daily drawdown risk.

Traders must monitor the portfolio dynamically and rebalance frequently.

Instead of fixed lookback windows, volatility is estimated adaptively—shorter during high volatility, longer during calm markets.

Forex pairs respond differently depending on global macro cycles. Risk parity can integrate regime detection models to allocate differently in “risk-on” vs “risk-off” markets.

ML models can predict volatility clusters, feeding into risk parity allocation. For example:

Assume a prop trader has $100,000 capital. They select 4 pairs:

Inverse volatility weights:

Final adjusted allocations:

Now, each pair contributes equally to total portfolio risk—protecting the trader from sudden shocks in USD/TRY or GBP/JPY.

Risk parity is not only quantitative—it also affects trader psychology.

Risk parity sits in the middle: practical, conservative, and adaptive.

For forex prop traders, building a risk parity portfolio is more than a theoretical exercise—it is a survival strategy. By ensuring each trade contributes equally to overall portfolio risk, traders reduce concentration risk, stabilize equity growth, and align with the stringent rules of funding firms.

Risk parity does not guarantee profits, but it maximizes risk efficiency, which is the ultimate currency for professional traders.

© 2025 iTrader Global Limited | Số đăng ký công ty: 15962

iTrader Global Limited có trụ sở tại Hamchako, Mutsamudu, Đảo tự trị Anjouan, Liên bang Comoros và được cấp phép, quản lý bởi Ủy ban Chứng khoán Comoros. Giấy phép số: L15962/ITGL.

iTrader Global Limited hoạt động dưới tên thương mại “iTrader” và được cấp quyền thực hiện các hoạt động giao dịch ngoại hối. Logo, thương hiệu và trang web của công ty là tài sản độc quyền của iTrader Global Limited.

Các công ty con khác của iTrader Global Limited bao gồm: iTrader Global Pty Ltd, số đăng ký công ty tại Úc (ACN): 686 857 198. Công ty này là đại diện được ủy quyền (số đại diện AFS: 001315037) của Opheleo Holdings Pty Ltd (giấy phép dịch vụ tài chính Úc AFSL: 000224485), có địa chỉ đăng ký tại: Tầng 1, số 256 đường Rundle, Adelaide, SA 5000.

Tuyên bố miễn trừ trách nhiệm: Công ty này không phải là tổ chức phát hành và không chịu trách nhiệm đối với các sản phẩm tài chính được giao dịch trên hoặc thông qua trang web này.

Cảnh báo rủi ro: Giao dịch CFD có mức độ rủi ro cao do đòn bẩy và có thể dẫn đến mất vốn nhanh chóng, không phù hợp với tất cả người dùng.

Giao dịch quỹ, CFD và các sản phẩm có đòn bẩy cao khác đòi hỏi kiến thức chuyên môn.

Nghiên cứu cho thấy 84,01% nhà giao dịch sử dụng đòn bẩy bị thua lỗ. Hãy đảm bảo rằng bạn hiểu rõ rủi ro và sẵn sàng chấp nhận mất toàn bộ số vốn trước khi giao dịch.

iTrader tuyên bố rằng họ sẽ không chịu trách nhiệm đầy đủ đối với bất kỳ rủi ro, tổn thất hoặc thiệt hại nào phát sinh từ hoạt động giao dịch có đòn bẩy, dù là đối với cá nhân hay pháp nhân.

Hạn chế sử dụng: iTrader không cung cấp trang web hoặc dịch vụ cho cư dân tại các quốc gia nơi hoạt động này bị cấm bởi pháp luật, quy định hoặc chính sách.